Numerous companies see the financial reporting process as nothing more than tracking financial numbers on paper. Although that may be true, in reality, financial reporting processes establish the foundation for producing clear, accurate data from day-to-day business activities that can be used to support informed strategic business decisions. These processes begin with data, proceed through stages of consolidation, verification, reporting, and approval, and conclude with the dissemination of information to relevant stakeholders. This same set of processes and systems is evident in MWDN projects, as reporting is often viewed as a monthly output rather than a continuous, process-based system. When a process-oriented methodology is followed, management has immediate access to all necessary information; however, when it is not followed, the leadership team is forced to use screenshots, improvised spreadsheets, or make promises such as “we’ll fix this by the next rollout.”

This is where most companies’ financial reporting fails. The problem is rarely a single mistake. It is a broken system related to numbers: fragmented source systems (ERP, billing, payroll, banking), spreadsheets that are manually passed between teams, different definitions (“gross profit” has three different meanings), and poor internal control of financial reporting, making it nearly impossible to justify what has changed, who approved it, and why. This is also where MWDN teams usually start: aligning definitions, ownership, and controls before automating anything. Last-minute consolidation between divisions and currencies forces even the best finance teams to put out fires instead of working on improving financial reporting.

The consequences are obvious: long closing cycles, unfounded confidence in the package, increased audit anxiety, and management acting on outdated, irrelevant, and/or inappropriate information. That’s why “more reports” usually doesn’t help. What does help is an automated reporting system with built-in accountability and control mechanisms, complemented by the right processes and tools.

Our experts, Vitalii Vystavnyi (CEO of MWDN) & Mykhaylo Merkulov (COO of MWDN) studied reporting teams in scale-up companies. There is a clear trend: the reporting issues are seldom attributable to a lack of tools. It’s a result of ambiguous ownership, absent controls, and automation in the middle of a mess.

In this guide, we will explain the various aspects of financial reporting in accounting and management, including objectives, purposes, and the most relevant frameworks, including basics of SEC financial reporting. We will define the practical aspects of ICFR, identify factors that may improve the quality of your reports, describe the ways in which the use of data analytics and AI in financial reporting can eliminate the need for repetitive tasks while protecting the organization from unanticipated exposures, and present a clear practical roadmap for reporting. We will outline criteria that help to assess financial reporting software, and explain when it is beneficial to engage financial reporting services to streamline the process.

What is financial reporting (and what it is not)?

Financial reporting covers the financial activities of an organization and transforms them into a consistent and repeatable set of reports that explain what happened, why it happened, and what it means for the business. Reporting, in the strictest sense of the term, means communicating financial results and financial position over a period of time, whether it be a month, quarter, or year. In reporting, an organization communicates its financial results and financial position in a way that is understandable and reliable to its stakeholders.

However, reporting is much more than just “sending financial statements”.

A complete set of financial statements consists of:

- 3 main financial statements (income statement, balance sheet, cash flow statement);

- accounting policy instructions & documentation, along with reference records on both non-recurring items, liabilities, and uncertainties;

- management discussion that transforms numerical data into operational issues (e.g., what changed, what improved, what became risky);

- operational KPIs that management uses alongside financial metrics (product margin, CAC/LTV, burn rate, revenue retention, cash reserves, inventory turnover, etc.).

Financial reporting is designed with the interests of two stakeholders in mind. Each stakeholder’s view of reporting from an academic perspective differs from that of the other.

External audience: trust and comparability

Investors, lenders, and regulators need to prepare their figures consistently and compare them across periods. This is where accuracy, disclosure, and audit trail are most important—especially when it comes to financing, loans, audits, or compliance.

Internal audience: decisions and speed

Actionable reporting is important for the following positions: founders, CFOs, FP&A managers, and product/operations managers. This information would tell the company where to invest, what to cut, which product lines are underperforming, if the margin of safety is tightening, and if cash is running out at an accelerated rate due to the timing of expenditures. The timeliness and detail of the internal report by segments will generally be faster, more detailed, and direct than the external report at providing an answer to the “why.”

What does “good” reporting look like?

High-quality financial reporting is not characterized by the most aesthetically pleasing design. It is characterized by signals that your team can trust:

- Timeliness: reports are provided early enough to be used, not two weeks after important decisions have been made.

- Accuracy: the numbers are balanced, assumptions are clear, and errors are identified and corrected well before the final report.

- Consistency: the meaning of the same metric is the same for all teams and reporting periods.

- Traceability: every figure can be traced back to its source, with approvals and an audit trail.

- Decision-making utility: it enables managers to make decisions, not just observe them.

This is where a financial reporting tool becomes more than just a “report generator”. The right tool provides repeatability: structured input, controlled changes, clear accountability, and a process that provides evidence of how the final report was generated. This is the foundation for reliable reporting at scale.

Financial reporting in accounting VS in management

In practice, companies use two reporting systems for the same transactions. They must be linked, but they are not the same thing. Understanding this difference allows you to make your business’s financial reporting scalable (and prevents endless discussions about “why don’t they match?”).

Financial reporting is not a single “monthly package”. In mature teams, it is divided into several levels that serve different purposes—compliance, operational decisions, and interpretation/action. Knowing which level you are building (and why) ensures consistency, scalability, and usefulness of reporting.

- Accounting reporting (“rule engine”)

- Management reporting (“operational model”)

- Financial reporting and analysis (“meaning level”)

MWDN POV: one reporting language before automation

Here are some financial reporting tips that we believe are most important before teams start working with tools:

✓ Identify a single metric owner

One metric per owner with a single definition source.

✓ Create connections across the organization

Establish a cohesive view of management and accounting.

✓ Stabilize the data model

Have a common understanding of how to measure and where that measure comes from.

✓ Finally, automate the process

As the definitions and responsibilities are finalized, automation will help add clarity instead of confusion.

Doing this will enable you to keep the accounting discipline in place while allowing for management to operate quickly and do not need to continually verify the numbers.

What is the objective of financial reporting (purpose, primary objective)?

Financial reporting’s purpose appears straightforward in words; however, it involves a complex process. Financial reporting provides the necessary information for decision-making and accountability. Reliable information means that the information must be explained (human contact) and that anyone can reproduce it (i.e., the data is available to anyone). Furthermore, this information must also be justifiable to others during an audit and to members of an organization when they want to know why margins have declined or whether or not they can execute a hiring plan.

That’s why the main goal isn’t “more detail”, but clarity at the decision-making level:

- Managers can confidently allocate capital and staffing levels.

- Investors and lenders can assess performance and risks.

- Teams can be accountable for the same reality (rather than different spreadsheets).

Every reporting team lives inside a triangle:

- Speed: how quickly the numbers are available after period end

- Accuracy: how correct and controlled the numbers are

- Completeness: how much context, segmentation, and narrative you include

All three cannot be at their peak simultaneously because this occurs during growth. Mature teams will intentionally manage this triangle.

Establish a strong and unyielding standard for accuracy with regard to total revenues, total cash, and major expense accounts.

Complete tiers of analysis will initially focus on a lean pack for speed. The second tier will segment into deeper levels with additional commentary.

Design the ability to repeat the process to improve speed and maintain control (i.e., same day each month for all of the following: owner, check, and sign-off).

This is where maturity of processes matters more than heroic deeds. Quick deal closing is not the merit of “strong people”. It is the merit of systems that reduce the amount of rework and prevent unexpected surprises.

Achieving goals through application

Reliable financial reporting will yield the greatest number of practical results:

1) Accurately forecasting: your forecasting will no longer be based on guesswork because you will have a reliable historical basis from which to work.

2) More straightforward financing: you’ll have a streamlined process for obtaining financing, accessing credit lines and communicating with your board without having to devote as much time and effort to defending yourself, as you will have documentation of your excellent track record.

3) Diminished audit problems: there will be considerably fewer last-minute adjustments to the numbers in the financial statement, an increase in the overall accuracy of the numbers presented, and significantly less time needed to demonstrate what occurred.

And this is where financial reporting can make sense. Not as “closing outsourcing”, but as accelerating the build of a reporting system. Defining a reporting model, developing controls, integrating data sources, automating consolidation, and ensuring repeatability of reporting as the business expands.

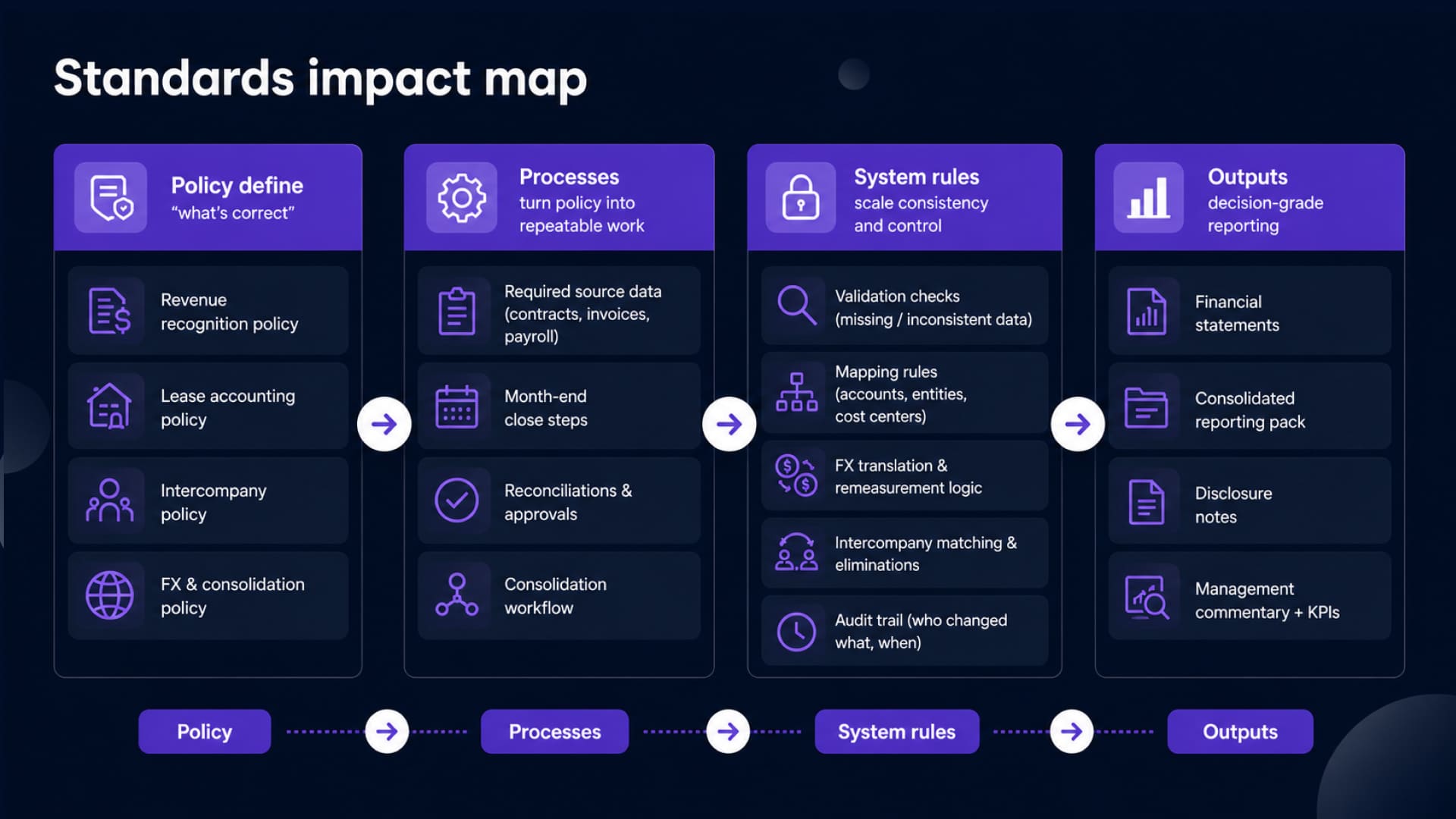

What are financial reporting standards (and why teams struggle with them)?

Reporting standards describe in detail what can and cannot be done when accounting for and presenting transactions that must be recognized, measured, and disclosed in financial statements. In this case, even the recognition of income and expenses, their measurement, presentation in financial statements, and explanation of notes for users are regulated by standards.

Why are standards operationally relevant?

Most teams view standards and treat them as something that belongs exclusively to the realm of finance, but standards transform operational processes by defining workflows that include typical scenarios such as:

- Revenue recognition (on delivery, over time, upon acceptance, based on policy and facts)

- Leasing (how lease liabilities and right-of-use assets are reflected in the balance sheet)

- Intercompany transactions (sales, loans, shared services, and services between entities)

- Foreign currency (what is revalued and what is translated, and where to recognize the gain/loss)

When systems cannot reflect the correct attributes according to contract terms, delivery stages, intercompany relationships, currency, and counterparty, the team manually closes this gap at the end of the period. This is a source of rework and inconsistency.

Consolidation and reporting: why having multiple reporting entities creates systemic problems

The greatest difficulties with standard reporting usually arise when multiple entities are involved in the process. Consolidation is not simply the “sum of the tables”.

It is a controlled process that includes:

- a single accounting policy within the group for identical transactions;

- the elimination of intra-group balances and transactions so that the group represents a single cohesive economic entity;

- the correct reflection of non-controlling interests and adjustments to ownership or control that occur over time, etc.

It is this complexity that makes consolidation a systemic issue, not just an accounting issue. There is a need for unified and consistent master data (business entities, charts of accounts, intercompany partners), repeatable exclusion logic, and an adequate and reliable mechanism for tracking adjustments.

Implications for tools

When there are a number of different entities and their standards don’t match up with the reality of organisational activities, the so-called “flexibility” of using spreadsheets goes away, and the use of spreadsheets introduces a high level of risk. Financial consolidation and reporting software provides value in this situation because it: encodes policy into repeatable, enforceable rules; reduces manual exceptions; and maintains traceability from the original source to the consolidated result.

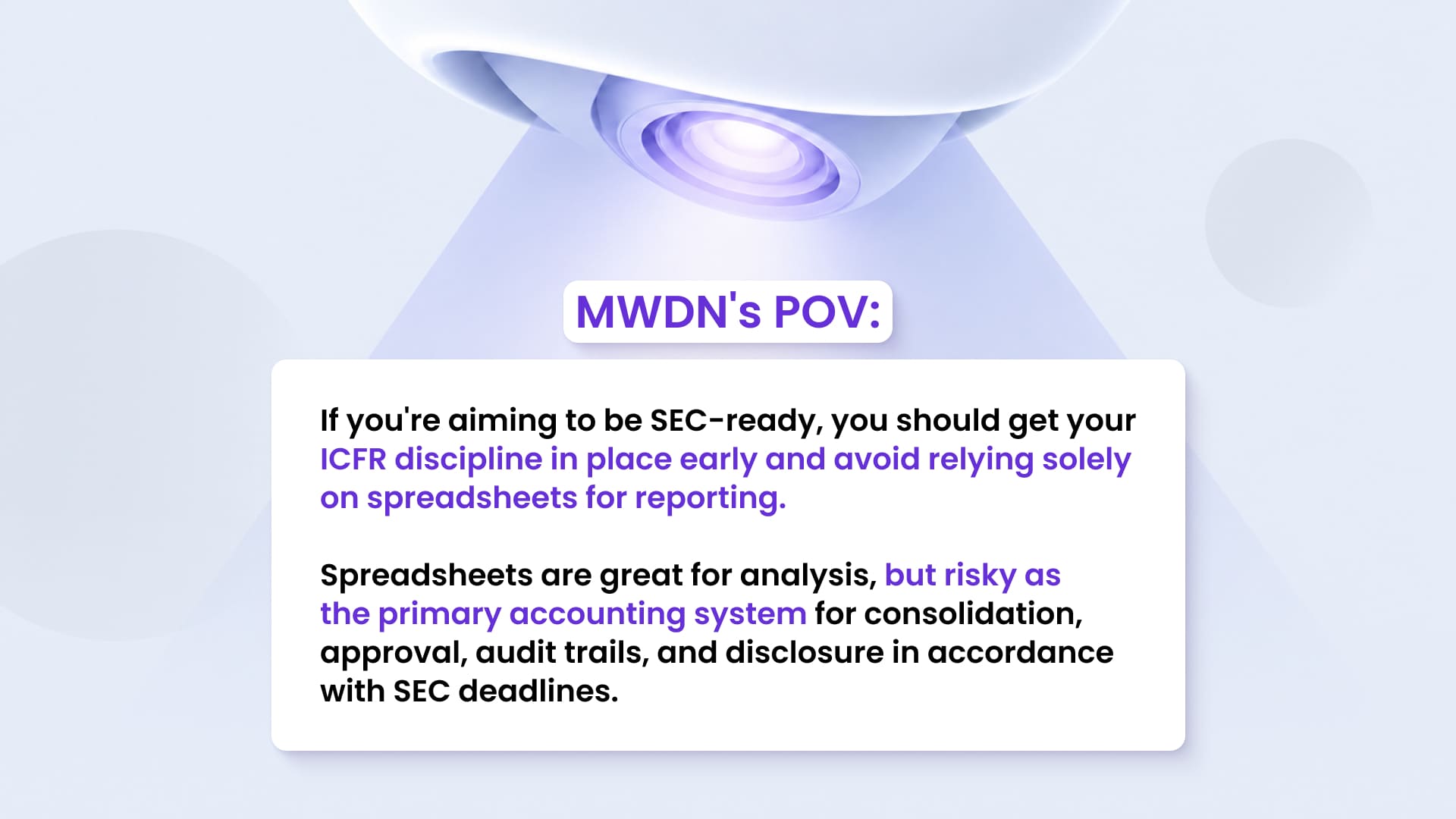

What is SEC financial reporting (and what changes if you’re public or planning to be)

SEC financial reporting is a requirement for US public companies to file periodic reports (most commonly the annual Form 10-K and quarterly Form 10-Q) with the US Securities and Exchange Commission. These documents contain financial statements as well as a significant amount of information about the business, risks, and disclosures, and they come with management responsibility: the CEO and CFO must certify key aspects of the reports.

The changes that occur once SEC reporting becomes part of your operations are not just about “more paperwork”. It’s a different standard of performance:

1) Deadlines are non-negotiable, and they are tighter than in most private deals

Deadlines for submitting documents depend on the status of the applicant, but the pattern is the same: tight deadlines and minimal tolerance for late corrections. Typical deadlines are 40-45 days after the end of the quarter for Form 10-Q and 60/75/90 days after the end of the year for Form 10-K, depending on whether you are a large accelerated, accelerated, or non-accelerated filer.

2) Expectations for disclosure are rising, and documentation is becoming part of the “product”

Regulatory submissions/information contained in an SEC filing needs to have well-supported documentation of each of its vital stats and descriptive statements (what was different, why it is different, and how you determined that it was different). The quality of financial reporting is determined by the level of measurable results (traceability, consistency, and significant/disclosure of information). All of this occurs under significant deadlines.

3) Control maturity must be scalable (ICFR is not optional)

Management is responsible for evaluating its internal control systems for financial statement preparation, and, depending on the level of company registration, independent auditors may be required to evaluate that assessment and/or provide independent confirmation of it.

4) “Closing + reporting” becomes cross-functional in its design

Submitting documents is not exclusively the prerogative of the finance department. It involves the finance department (numbers), legal department (disclosure), audit/audit committee (governance), and business data owners (core operational data). You can view this as a workflow problem, or suffer through it as a series of constant fire drills.

What is internal control over financial reporting (ICFR) and why it’s non-negotiable?

Internal control over financial reporting (ICFR)

is a system of policies, procedures, and controls that provides “reasonable assurance” that your financial reports are reliable, meaning that the figures are complete, accurate, approved, and traceable to evidence. ICFR exists because financial reporting is not just about calculations. It is also about managing risk: preventing errors, identifying problems early, and confirming how the final figures were arrived at.

What is control: preventive + detective?

In practice, control is divided into two categories:

- Preventive control prevents problems from arising before they appear in reports (e.g., access restrictions, required approvals, verification rules).

- Detective control detects problems after they occur (e.g., reconciliations, exception reports, deviation checks).

A mature ICFR system uses both types. Preventive controls reduce the amount of rework. Detective controls protect you from “silent failures” when something breaks in the data flow.

Typical ICFR control areas (what teams implement in real life)

- Access & segregation of duties

- Approval workflows

- Reconciliations

- Change management (especially for reporting logic)

- Audit trail and evidence

- Limit the number of people who can create suppliers, change bank details, publish journal entries, or change reporting schemes. Separate the responsibilities of “creation”, “approval”, and “release” so that one person cannot enter and hide an error.

- Key transaction approval stages: journal entries, manual adjustments, revenue recognition exceptions, write-offs, and consolidation entries. Approvals create accountability and reduce the “we’ll remember why later” problem.

- Regular reconciliation of cash, accounts receivable/payable, payroll, intercompany balances, and major subsidiary ledgers. Reconciliation is a control that confirms that your totals are accurate and not just the latest status of the system.

- Any changes to mapping rules, consolidation logic, currency conversion, KPI formulas, or reporting templates must be verified, tested, and recorded. Reporting logic is hidden code. Neglecting it will result in “the numbers changing, and no one knowing why”.

- ICFR requires evidence: who approved it, what supporting files exist, what corrections were made, and why they were made. This is what makes reporting reasonable during an audit, inspection, or control by the board of directors.

Why “automation without control” accelerates errors?

This is what teams learn, often painfully, from their own experiences: automation can only scale what already exists. Should the data input be in a random or baffling state, unclear responsibility for this should be assumed, and poor change control will have been implemented. Financial reporting’s automation may give speed but not necessarily reliability. Worse comes to worst when you have speed, but not trust.

How to improve financial reporting (quality, speed, confidence)?

Improving reporting is not about adding new tabs or performance metrics. It is about building a system that will remain reliable as the company grows. The fastest improvements are achieved by first fixing the input data and rules, then strengthening the closing process, and only then scaling up with tools. This way, you will improve the quality of financial reporting without turning closing into a monthly crisis.

Our team has prepared a “Reporting quality checklist”, so it is easy for you and your team to handle the bottlenecks.

When all the ticks ✓ are in place, your financial reporting quality becomes stable.

How data analytics can help financial reporting?

Basic reporting tells you what happened. But it’s data analytics that helps you understand what is unusual, what is driving change, and where it is happening. This is the difference between a reporting package that is simply stored in an archive VS a reporting system that actually influences decision-making.

What analytics adds beyond basic reporting?

1) Detecting anomalies (cases that fall outside the norm and unexpected changes)

Analytics can detect patterns that do not correspond to the normal state of your business: a sudden drop in margins in one region, duplicate revenues, unusual refunds, or a sharp increase in expenses in the wrong cost center. This is not “higher mathematics”. It is the systematic identification of exceptions: determining what deviates from expected ranges, trends, or relationships (e.g., revenue growth with no change in cash inflows).

This is where AI is usually first applied in financial reporting. Not as a replacement for finance, but as a way to identify anomalies more quickly and ask the right questions to the right owners.

2) Analysis of factors (explaining deviations)

Monthly deviation is only useful if it is broken down into its constituent factors.

Analytics helps break down changes into understandable components:

Instead of “Marketing costs increased”, you get

“Costs increased because the paid search budget increased in two geographic regions, CPC increased by 12%, and conversions fell by 6%, net CAC increased by 18%”.

3) Segmentation (where the change occurs)

Analytics makes reports useful by breaking down total amounts into parameters that managers actually control:

Thus, a single “margin decline” becomes a specific problem “The margin for product B in the average EU market has declined due to discounts and higher costs to support a single customer”.

Where analytics lives (and why it matters)

There are many different possible positions for analytics in an organization, based upon the legacy application architecture or technology stack, the company’s level of analytics maturity, and the nature of the particular analytics utilization requires:

- BI layer (dashboards + semantic models): great for quick breakdowns, visual trend checks, and self-service exploration.

- Data warehouse/data lake: best suited when you need consistent modeling, history, and consolidation of multiple sources (billing + product + finance + CRM).

- Built into financial reporting software: useful when analysis is closely tied to closed workflows, consolidation logic, and controlled reporting packages.

The key is not “where it is”, but whether the results can be traced: can you link the chart to the source transactions and approved definitions?

MWDN POV: analytics is only as good as definitions and data lineage

Analytics isn’t the answer to reporting chaos; it actually makes it worse.

When different teams define their own notions of “revenue,” analytics produces powerful-looking yet contradictory charts. In the absence of a defined data source, anomalies are debated rather than investigated. The fastest teams establish definitions, responsibilities, and data provenance; analytics then becomes a driving force for decision-making in reporting.

AI in financial reporting (including NLG for financial reporting)

AI can be really useful in finance, but only when it is used as an assistant in a controlled reporting system. The goal is not to “entrust AI with reporting.” The goal is to reduce manual work while improving the speed and quality of financial reporting: fewer errors, clearer explanations, and faster review cycles.

What AI can safely do (when controls are in place)?

1) Assistance with classification suggestions

AI can identify and recommend matching accounts/categories for your transactional entries (e.g., supplier expense categories or the type of expense they may belong to). This is most effective when a model is built on your chart of accounts, historical matches, and well-defined rules, and exception handling is the responsibility of a human owner. This allows you to perform repetitive tasks quickly and reduce labor costs without changing ownership.

2) Identifying anomalies and inconsistencies

Among the top benefits of applying AI within a financial reporting context is the capability of detecting outlier behaviours that require investigation; these can include remarkable fluctuations in expenditure, repeated journal entries, differing revenue records from operating ratios, or inconsistency across related entities. AI will alert organizations regarding these issues, while individuals must interpret what they mean and how to correct them.

3) Draft commentary on deviations (NLG) with human review

The application of NLG to financial reporting is an area where AI is often perceived as being “magical” and where teams can save a significant amount of time. Rather than having to write the same commentary from scratch each month, AI can generate standard-style commentary that identifies changes, drivers of change, one-off items, recurring items, and what to expect next month.

But the commentary must be reviewed and approved, as descriptive text can create risk even if the numbers are correct.

What AI should not “own” on its own?

AI should not be the final authority on the following issues:

- Final figures (published amounts, consolidations, adjustments)

- Compliance statements (statements such as “fully compliant”, “in accordance with X” without management)

- Uncontrolled external statements for filing, investors, or regulators

The areas mentioned above need to have clear accountability, evidence, and approval in place. By allowing AI to alter results without strict controls, you will receive quicker reporting; however, this could result in less trust.

Practical controls that make AI safe in finance

If you want AI in reporting without creating new risk, the controls are not optional:

| Control | What it means in practice | Why it matters |

|---|---|---|

| Approvals & sign-offs | Every AI-assisted reclassification, adjustment suggestion, or narrative draft has a named reviewer and an approval step. | Keeps accountability with humans and prevents “auto-published” mistakes. |

| Prompt governance (standard prompts, locked templates) | Treat prompts like reporting logic: use approved templates and block ad-hoc “creative” prompting for anything that impacts official reporting. | Ensures consistency and reduces unexpected outputs. |

| Data access rules | Limit what AI can see with role-based access; don’t expose sensitive data to users who wouldn’t normally have it. | Reduces confidentiality risk and prevents data leakage. |

| Logging & auditability | Log inputs used, outputs generated, edits, and approvals (who/when/what). | If you can’t trace it, you can’t defend it, especially under audit or diligence. |

MWDN’s POV:

Only with accountable and defined criteria for reporting and trustworthy genealogy does AI improve the reporting process. Without these criteria in place, AI provides assurance that is not verifiable, which is the opposite of what constitutes quality reporting in finance.

How to automate financial reporting (and choose the right setup)?

Automation only works when it follows a clear reporting system: defined input data, controlled logic, and repeatable output data. In practice, “financial reporting automation” is not a single function.

It is a chain: collection → verification → consolidation → publication → monitoring.

The stronger the chain, the higher the reporting speed and trust without losing control.

Step-by-step roadmap: from manual close to automation

First, start with a list of what actually drives the numbers: ERP/GL, billing, payroll, banking, and often CRM.

The goal is not to “connect everything”. The goal is to identify the systems that hold the truth about revenue, expenses, cash, and headcount, and stop duplicating the same data in multiple places.

Then, document the metrics that have value for analysis; some examples of these metrics would be: entity, currency, product, client segment, cost center, country/region, and channel. If these attributes are not established and governed, you will continue to spend time on completing the same reporting in multiple formats.

Once you have more than one entity, consolidation creates a systemic issue – such as reconciling between different entities, eliminations, currency translations, and consolidation entries. If this logic is contained solely in spreadsheets, every month will become a separate “project”, and your traceability may become inconsistent. At this point, using financial consolidation and reporting software is more of a necessity than a luxury.

Also, automation must have controlled checks that provide certainty around completion of accounting processes, that comply with standards, and that provide for exception processing. If you automate your accounting work without implementing this type of control level, you will improve the speed of execution; however, you will sacrifice the integrity of your financial reporting.

Moreover, a mature system generates both financial reports and management packages (KPIs, segment reviews, variance tables). Descriptions can be created using NLG, but they always need to be reviewed. This is where automated financial reporting software and financial reporting automation tools pay off: repeatable results with less manual formatting and fewer edits later in the cycle.

Finally, many teams fail to monitor and wonder why their reporting continues to decline over time. Monitoring is the submission of alerts for missing channels, on-time tasks, broken conformances, and unexpected changes. Furthermore, monitoring gives you the utility of keeping a record of what has changed and when.

How to choose the best financial reporting software (what “best” really means)

The best financial reporting software is not a brand name. It is the match between your reporting reality and your control requirements.

Use these criteria to choose a financial reporting tool without creating new reporting chaos:

- Number of entities: single entity consolidation vs. multiple entity consolidation

- Consolidation complexity: intercompany transactions, eliminations, foreign currency transactions, ownership changes

- Audit/compliance requirements: disclosure workflows, evidence, approvals, audit trail maturity

- Required integrations: ERP + billing + payroll + banking + BI/warehouse

- Disclosure/disclosure workflows: controlled comments, versions, reviewer roles

- Permissions and traceability: who can change mappings, logic, templates, and how it is logged

Typical failure mode: purchasing a tool before defining ownership, mappings, and reporting logic. The result is usually “we implemented the software, but we’re still closing in spreadsheets”.

When financial reporting services make sense (and what to outsource)

When your sales deals are taking longer than they should take to close, require significant revisions of numbers, and your management has no belief that they can trust your team; the problems that you are experiencing are typically not due to “too few people,” but to a lack of systematic capabilities; which include good definitions for inputs, the ability to apply consistent logic to data, and a process that is capable of being repeated over time. Companies that offer financial reporting services can assist in developing those types of systems much quicker than your internal capabilities can, allowing you to develop a process for collecting/reporting financial information without creating a continued dependence on outside consultants.

Phase 1 Diagnose (1–2 weeks)

Goal → align on what “correct” and “useful” mean, and identify where the close breaks.

What happens

✓ Map data sources and owners (ERP/GL, billing, payroll, banking, CRM/BI where relevant)

✓ Confirm KPI definitions and reporting rules (one definition per metric)

✓ Identify close bottlenecks, control gaps, and recurring failure points

Deliverables

✓ Target-state reporting blueprint (process + controls + tooling)

✓ Quick-win list (what can be fixed immediately vs what needs a build)

Phase 2 Build (2–6 weeks)

Goal → convert the blueprint into a repeatable reporting system.

What happens

✓ Implement the reporting data model and mappings (entities, currencies, dimensions)

✓ Set up consolidation logic when needed (intercompany matching, eliminations, FX rules)

✓ Add validations, approvals, and audit trail requirements (ICFR-friendly workflow)

✓ Automate repeatable outputs: statements + management pack + controlled narrative drafts

Deliverables

✓ Stable close workflow with defined gates and evidence

✓ First automated reporting pack that reconciles end-to-end

Phase 3 Scale (ongoing / optional)

Goal → keep reporting strong as the company grows, systems change, and complexity increases.

What happens

✓ Add dashboards and deeper segmentation (product/region/customer cohorts)

✓ Introduce monitoring (missing feeds, broken mappings, late tasks, anomaly alerts)

✓ Document logic and hand over ownership (so the system doesn’t degrade)

Deliverables

✓ Reporting that stays timely and trustworthy quarter after quarter

✓ Clear ownership model (who maintains mappings, who approves changes, who reviews exceptions)

Conclusion

The article illustrated that financial reporting is an operating system instead of a collection of reports; as such, when the financial reporting process is designed as a re-occurring flow of data → consolidate → controlled → described → approved → stakeholders, managers are able to make business decisions based on timely information supplied by the financial reporting system. However, when this flow is not in place, teams are given disparate tables and conflicting definitions, reactive last-minute consolidations, and weak internal controls over financial reporting (ICFR), all of which contribute to a lack of trust in the accounting process and a continual cycle of fire drills at the end of each month.

The basic idea which we wanted to talk remains the same: tools alone do not solve the reporting problem. Reporting quality improves when companies first define and assign responsibility for the various components of reporting, then develop a “closed” process with built-in controls and evidence, and only then scale it with analytics and artificial intelligence.

MWDN helps companies that require fast, reliable reporting in phases of rapid multi-entity growth, preparation for audit or fundraising, or when preparing for SEC compliance by providing standard delivery solutions such as designing the reporting system, consolidation logic, ICFR-ready controls and audit trail creation, integration with ERP/Billing/Payroll/Banking/Business Intelligence/Warehouse systems, automation of the reporting process, documenting the reporting processes, and creating a clear responsibility matrix.

If you need assistance determining whether your reporting issue is caused by tooling, process, or control problems, contact us and we will discuss your current reporting process, look for the weak points, and determine the next safest step to automate.

FAQ

How do I know if my company needs financial reporting automation or just a better reporting process?

If your team still spends most of the close cycle collecting files, checking formulas, reconciling different spreadsheet versions, or explaining why the same metric has different values in different reports, the problem is usually not only about software. Financial reporting automation works best when your data sources, metric definitions, ownership, approval steps, and control points are already clear. Without this foundation, automation may only make the same errors faster and harder to trace.

MWDN helps companies understand whether the reporting issue comes from tooling, process design, data structure, or weak controls. Our team can map the current reporting flow, identify where delays and inconsistencies appear, define the right target-state process, and only then recommend what should be automated first.

Can financial reporting software replace my finance team?

Financial reporting software can reduce manual work, improve traceability, speed up consolidation, and make reports easier to review. However, it cannot fully replace finance ownership. Someone still needs to define reporting rules, review exceptions, approve changes, interpret results, and make sure the final numbers are accurate, compliant, and useful for business decisions. The strongest setup is usually a controlled system where software handles repeatable work, while finance keeps responsibility for judgment, approval, and interpretation.

MWDN does not approach financial reporting automation as a “replace people with tools” project. We help companies build reporting systems where finance teams spend less time on repetitive formatting, manual checks, and data collection, and more time on analysis, planning, and management-level decisions.

What should I prepare before choosing financial reporting software?

Before choosing a financial reporting tool, it is important to understand how complex your reporting really is. Key factors include the number of entities, currencies, ERP or accounting systems, consolidation rules, intercompany transactions, required approvals, audit trail expectations, and the level of reporting detail your management needs. If these areas are not defined before implementation, even strong software can turn into another layer of manual work.

MWDN can help prepare this foundation before tool selection or implementation. Our team defines data sources, reporting dimensions, ownership, control logic, integration needs, and automation priorities so the selected software supports the actual reporting process instead of creating more operational complexity.

How can AI be used in financial reporting without creating compliance risks?

AI can support financial reporting by detecting anomalies, suggesting transaction classifications, helping draft variance commentary, and identifying unusual patterns in expenses, revenue, or margins. But AI should not own final figures, compliance statements, consolidation adjustments, or investor-facing reporting without human review. To use AI safely, companies need approvals, access rules, prompt governance, logging, auditability, and clear responsibility for every AI-assisted output.

MWDN helps companies introduce AI into reporting carefully, with controls built into the process from the start. We can support AI-assisted workflows for anomaly detection, commentary drafting, and reporting checks while keeping human review, evidence, and accountability at the center of the system.

When should I involve an external team for financial reporting services?

External financial reporting services make sense when internal teams are overloaded by monthly closing, reports take too long to prepare, numbers often require rework, or management does not fully trust the reporting package. They are also useful before audits, fundraising, multi-entity expansion, or SEC-readiness projects, where reporting needs to become more structured, traceable, and repeatable.

MWDN can step in to diagnose reporting bottlenecks, design a target reporting model, set up consolidation logic, connect ERP, billing, payroll, banking, BI, or warehouse systems, and build automated reporting workflows. The goal is not to create dependence on external consultants, but to help your company build a reporting system your internal team can trust and maintain.