In labor and taxation legislation, “Per Diem” refers to a daily allowance or payment that is typically provided to employees or individuals to cover expenses incurred while traveling for work-related purposes. The term “Per Diem” is derived from Latin, meaning “per day.”

Sometimes, the term “per diem” also denotes a daily payment model for temporary or on-demand jobs, such as for locum nurses or relief teachers, however, this meaning is not a subject of the following article.

Key aspects of Per Diem

In the context of labor and taxation legislation, Per Diem includes:

Travel expenses

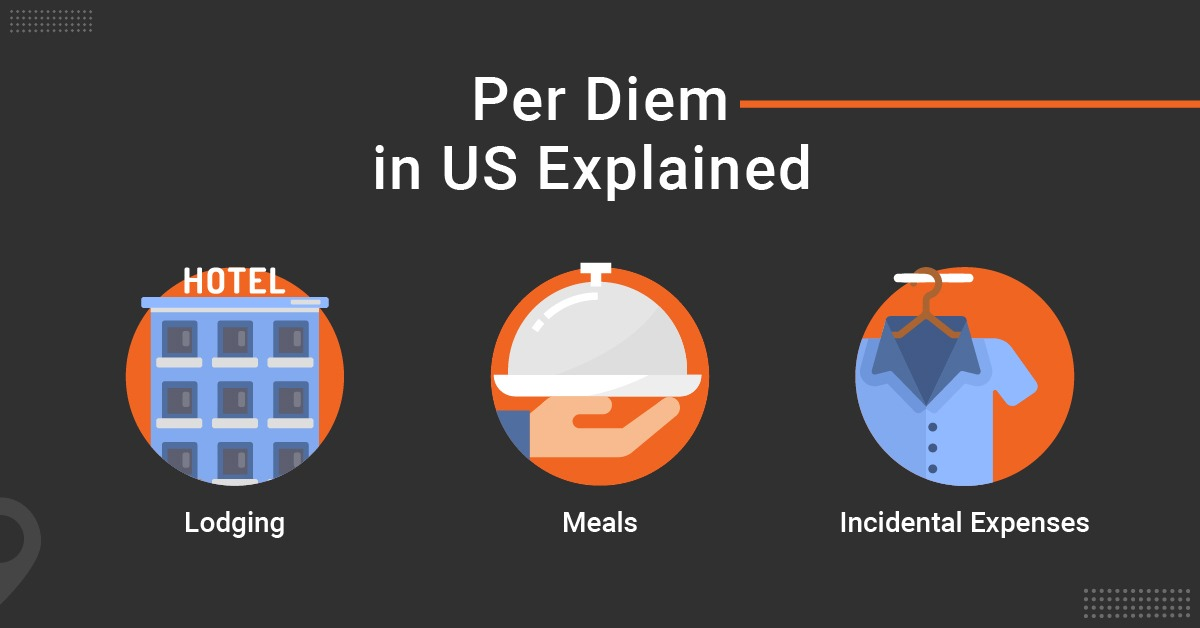

Per Diem is intended to cover expenses for meals, lodging, transportation, and incidental expenses that employees or individuals may incur while away from their usual place of work. It simplifies the reimbursement process by providing a fixed daily allowance rather than requiring employees to submit receipts for each expense.

Fixed rates

Per Diem rates can vary by location and are often set by government agencies or employers based on local cost-of-living and business travel considerations. These rates may be different for domestic and international travel.

Taxation

Per Diem payments can have implications for income tax purposes. In many countries, including the United States, the tax treatment of Per Diem depends on whether the payment is considered accountable or non-accountable.

Under an accountable plan, Per Diem payments are not included as taxable income for the employee. However, the employee must provide an expense report detailing each expenditure’s time, place, and business purpose. Any unused funds are typically returned to the employer.

If Per Diem payments don’t meet the requirements of an accountable plan, they may be treated as taxable income, subject to withholding and reporting, and are called non-accountable.

Both employers and employees should be well aware of the specific regulations and guidelines regarding Per Diem in their jurisdictions. Failure to comply with tax and labor laws related to Per Diem can lead to tax liabilities and legal issues. Therefore, many organizations have well-defined Per Diem policies to ensure proper compliance and documentation.

Limits, regulations, and specific rules

Some countries and employers impose limits on Per Diem rates to prevent excessive or inappropriate expenses. Additionally, regulations may specify when Per Diem can be provided, such as during business travel but not for regular daily commuting.

Certain industries, such as the trucking and construction sectors, have specific Per Diem rules and rates due to the nature of their work, which often involves extensive travel and lodging expenses.

Employers and employees must maintain accurate records of Per Diem payments and related expenses to ensure compliance with tax and labor laws.

When employees travel internationally, Per Diem rates can vary significantly between countries, and currency exchange rates may also affect the calculation of daily allowances.

How to work out Per Diem?

Per Diem amounts are predetermined daily rates given to staff for business-related travel expenses. Issuing these rates simplifies expense tracking and negates the need for extensive expense reports or receipt collections. The organization’s travel guidelines should provide clear directives on per diem provisions.

To compute per diem: (1) ascertain the organization’s Per Diem rates; (2) verify the eligible days (and nights) of travel; (3) multiply the per diem rate with the number of days.

For instance, let’s consider a sales representative traveling for three days, with a two-night hotel stay, to conduct training and sales pitches. Given a daily travel allowance of $50 and a hotel rate of $150 per night:

($150 x 2 nights) + ($50 x 3 days) = $450

In the U.S., firms can take cues from the GSA to determine federal per diem rates. Updated annually, these rates factor in lodging costs, food expenses, and other variables.

Per Diem: by day or night?

Per diem allocations differ based on the nature of expenses. Daily Per Diem covers meals, commuting, and other daily costs. Nightly Per Diem addresses accommodation costs.

Tax aspects of Per Diem

In the U.S., Per Diem is generally tax-exempt. However, specific scenarios can have tax implications, as directed by the IRS. Typically, Per Diem becomes taxable if it surpasses the federally set Per Diem cap. If it exceeds this limit, only the excess amount becomes taxable.

Under specific conditions, employees can avail tax deductions on per diem, especially if adhering to GSA rates. Though the IRS allows businesses to deduct legitimate employee travel expenses, companies must maintain a verifiable plan to substantiate these deductions.

***

Reimbursing business-related expenses is crucial for maintaining employee satisfaction and mutual trust. At MWDN, we facilitate a seamless experience for finance departments, ensuring international compliance.